|

Workers' compensation insurance, commonly called workers' or workmen's comp, is a form of insurance designed to provide compensation to workers who have been injured while on the job.

While the details can vary significantly from one plan to the next, insurance plans in this category typically provide for some form of wage replacement, payment and/or reimbursement of medical costs, compensation for economic losses, possibly damages for pain and suffering, and settlements to the insured's dependents in the case of a fatal work-related accident.

0 Comments

Q: I’ve seen several Professional Employer Organizations (PEOs) promote a "cost savings" for business owners for signing up with their program. They advise that by risk pooling with other employers, their Workers Compensation rates are greatly reduced and this savings is passed along to their clients.

Could someone who is affiliated with one of these companies please clarify? A: PEO's are best suited to offer "cost savings" for businesses with high experience mods or high-risk operations. In addition, PEO's can offer greater credits in states that otherwise restrict premium credits (i.e. New Jersey, Florida) or where territorial rating factors play a role (i.e. Los Angeles County). In essence, PEO's are a loophole that do not need to directly abide by statutory workers' comp rating rule. That being said, I do have two stipulations with PEO's. First, it is best to work with reputable, financially stable, and long-standing companies, who preferably own their workers' compensation insurance carrier. Second, it is best to work with a PEO that maintains the clients experience mod. Some (if not most) PEO's lump the clients employees in a mass policy so no payroll is run under the actual company. In doing so, the experience modification "freezes" which makes it harder for the company to leave the PEO in the future and more importantly the company loses its ability and benefits of reducing their experience mod. Are you unhappy with your current Workers Compensation Insurance coverage and want to cancel your policy before the effective date? Fortunately, you do have a choice! This article can help you decide if a mid-term switch would be benefit your business.

Professional Employer Organization services are an excellent way to reduce the cost of your workers' compensation premium while benefiting from payroll administration and processing, employee benefit offerings, accelerated risk management, and human resources support.

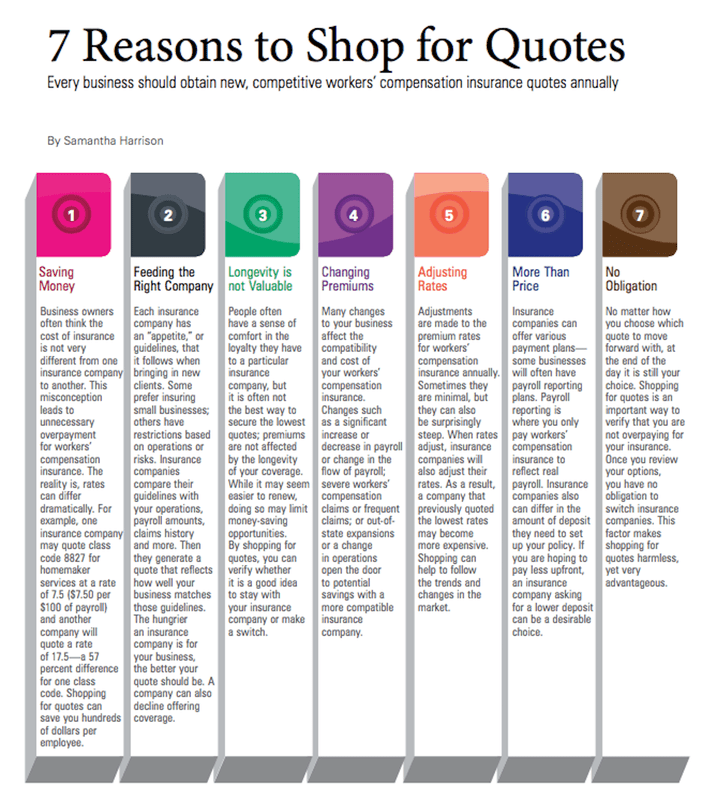

This happy client at Chief Insurance Solutions, LLC saved over 35% off her Workers Compensation Insurance premium and learned the value of shopping each year for Workers Comp quotes. She learned how rates change each year, giving her business the opportunity to save money by switching carriers.

Being prepared for your Workers Compensation Audit is not something to think about right before your Audit is scheduled, but something to plan for in advance. The information below is generally requested at the time of your physical Workers Compensation Audit. Having these records well organized throughout the year reducing the hassle of preparing for the Audit and simplifies the process.

|

AuthorChief Insurance Solutions LLC - Expert Advisor Categories

All

|

RSS Feed

RSS Feed